Understanding the Mortgage Process for Lenders

The mortgage process is a multifaceted journey involving various stages, each crucial for both lenders and borrowers. Understanding this process is essential for lenders aiming to provide excellent service while ensuring compliance and efficiency. This guide delves into the key stages, challenges, and important documents that play critical roles in the mortgage process for lenders.

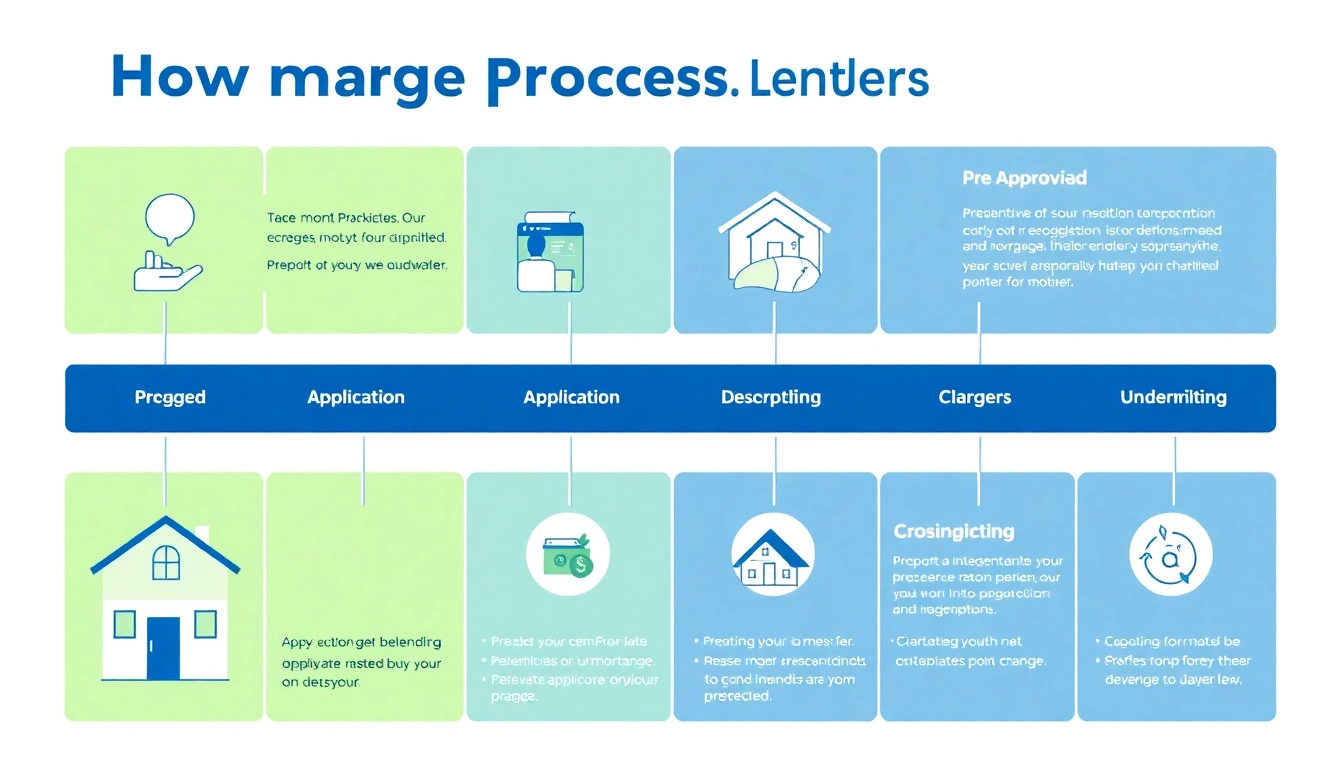

Key Stages in the Mortgage Journey

The mortgage lending process can be divided into several key stages. Each of these stages requires specific actions and documentation, aimed at evaluating the borrower’s eligibility, assessing the collateral, and facilitating the closing of the loan. Here’s an overview of these stages:

- Pre-Approval: This initial step involves assessing the borrower’s financial status to determine how much they can afford to borrow.

- House Shopping: After pre-approval, borrowers typically search for properties within their price range.

- Mortgage Application: Once a property is found, the borrower submits a formal application for the mortgage.

- Loan Processing: Lenders gather and verify relevant documentation related to the borrower and the property.

- Underwriting: The loan application is thoroughly examined to assess risk and make the final decision on approval.

- Closing: The final paperwork is processed, and ownership of the property is transferred to the borrower.

Documents Needed for Mortgage Applications

For lenders, having a clear understanding of the necessary documentation for mortgage applications is crucial. The typical documents required include:

- Proof of Income: Pay stubs, tax returns, and W-2 forms to establish earning stability.

- Credit History: Credit reports to assess the borrower’s creditworthiness.

- Asset Verification: Bank statements or investment account statements to demonstrate available funds.

- Identification: Government-issued ID to verify the identity of the applicant.

- Property Information: Details about the property, including the purchase agreement and property disclosures.

Common Challenges Faced by Lenders

Lenders encounter numerous challenges throughout the mortgage process. Some of the common issues include:

- Documentation Delays: Incomplete or late submission of documents can halt the process.

- Market Fluctuations: Changes in interest rates can impact the affordability of loans.

- Regulatory Compliance: Adhering to the myriad of lending laws can be complex and time-consuming.

- Underwriting Variability: Different underwriters may assess the same application differently, leading to inconsistencies.

Getting Pre-Approved: Starting the Mortgage Process

Pre-approval is a pivotal element of the mortgage process, laying the groundwork for both the lender and the borrower. It establishes an initial trust and framework for the transaction.

Benefits of Pre-Approval for Lenders

Pre-approvals provide numerous advantages for lenders, including:

- Streamlined Processes: Having pre-approved clients can expedite the lending process significantly.

- Stronger Lead Conversion: Pre-approved borrowers are often more serious buyers, increasing the likelihood of closing deals.

- Risk Assessment: Understanding a borrower’s financial status helps in assessing risk and tailoring loan products appropriately.

Steps to Secure Pre-Approval

To obtain a pre-approval, lenders typically require borrowers to follow several steps, including:

- Gathering financial documents, such as tax returns and pay stubs.

- Submitting an application detailing their financial situation.

- Undergoing a credit check to determine creditworthiness.

- Receiving a pre-approval letter indicating the maximum loan limit.

Timeframes for Pre-Approval

The pre-approval process can vary in duration, generally taking anywhere from a few days to a couple of weeks, depending on the lender’s processes and the completeness of the borrower’s documentation. Quick turnaround times are often sought after to enhance client satisfaction and competitiveness.

Completing the Mortgage Application

Once pre-approval is secured, the next step is the formal mortgage application. This aspect is critical as it significantly influences the lending decision.

Essential Elements of a Strong Application

A strong mortgage application should encompass several essential elements:

- Complete Personal Information: Including social security numbers, addresses, and employment details.

- Financial Statements: Providing a clear picture of assets and liabilities.

- Credit Report Consent: Allowing lenders to access credit information.

- Property Details: Information regarding the property being purchased.

How Lenders Evaluate Applications

Lenders evaluate mortgage applications through a detailed review process, which includes:

- Creditworthiness: Analyzing credit scores and payment histories.

- Debt-to-Income Ratio: Calculating the borrower’s monthly debt obligations against their gross monthly income.

- Employment Stability: Assessing job history and current employment status for reliability.

Tips for Improving Application Success

Lenders can help borrowers improve their application success by providing the following tips:

- Encouraging borrowers to check their credit scores before applying.

- Highlighting the importance of a stable job history.

- Recommending that borrowers reduce their debt-to-income ratio by paying down existing debts.

Navigating Underwriting and Approval

After submitting the mortgage application, the next stage is underwriting, where the application undergoes rigorous examination.

The Underwriting Process Explained

Underwriting involves a comprehensive review of the loan application, including the verification of income, assets, debt obligations, and property value through various checks, including:

- Property Appraisal: Evaluating the property’s market value to ensure it meets the loan amount.

- Risk Assessment: Identifying potential risks based on a borrower’s financial condition.

- Verification of Information: Confirming the accuracy of all submitted documents.

Timeline Expectations for Lenders

The underwriting process typically takes one to three weeks, but factors such as the complexity of the loan and the busy seasons can impact this timeline. Clear communication with borrowers about potential delays is crucial for maintaining trust and customer satisfaction.

Understanding Common Underwriting Conditions

Once underwriting is completed, lenders may issue conditions that borrowers need to address. Common conditions may include:

- Providing additional documentation, such as bank statements or tax returns.

- Clarifying details within the credit report.

- Resolving any discrepancies found during the verification process.

Closing the Deal: Final Steps in the Mortgage Process

The closing process marks the culmination of the mortgage journey, where all final steps are completed to finalize the loan.

What to Expect During Closing

During the closing, both the lender and borrower must be prepared to complete several steps:

- Review of Closing Disclosure: The lender discloses all financial details, such as loan terms and closing costs.

- Signing Documents: Both parties sign the necessary documents to finalize the loan.

- Funding the Loan: After signing, the lender will fund the loan, making it available for use.

Important Documentation for Closing

Several documents are essential for the closing process, including:

- Loan Agreement: Outlining the terms and conditions of the mortgage.

- Closing Disclosure: Providing an itemized list of all closing costs.

- Title Documents: Ensuring that the property title is clear from any liens.

- Insurance Proof: Documenting that homeowners insurance is in effect before closing.

Post-Closing Activities for Lenders

After closing, the lender’s responsibilities include managing the mortgage, collecting payments, and addressing any ongoing customer service needs. It’s also important for lenders to ensure that all relevant records are maintained according to compliance and regulatory standards.